From Wikipedia, the free encyclopedia

Blogger Ref Link http://www.p2pfoundation.net/Transfinancial_Economics

The term macroprudential regulation characterizes the approach to financial regulation aimed to mitigate the risk of the financial system as a whole (or "systemic risk"). In the aftermath of the late-2000s financial crisis, there is a growing consensus among policymakers and economic researchers about the need to re-orient the regulatory framework towards a macroprudential perspective.

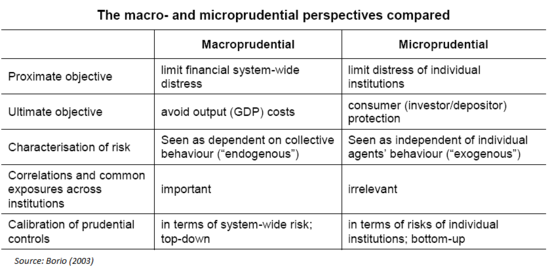

Differences between macro- and microprudential approaches (Source: C. Borio, 2003).

Differences between macro- and microprudential approaches (Source: C. Borio, 2003).

The agency paradigm highlights the importance of principal-agent problems. The main argument is that in its role of lender of last resort and provider of deposit insurance, the government alters the incentives of banks to undertake risks. This is a manifestation of the principal-agent problem known as moral hazard. More concretely, the coexistence of deposit insurances and insufficiently regulated bank portfolios induces financial institutions to take excessive risks.[6] This paradigm, however, assumes that risk arises from individual malfeasance, and hence it is at odds with the emphasis on the system as a whole which characterizes the macroprudential approach.

In the externalities paradigm, the key concept is called pecuniary externality. This is defined as an externality that arises when one economic agent's action affects the welfare of another agent through effects on prices. As argued by Greenwald and Stiglitz (1986),[7] when there are distorsions in the economy (such as incomplete markets or imperfect information[8]) policy intervention can make everyone better off in a Pareto efficiency sense. Indeed, a number of authors have shown that when agents face borrowing constraints or other sorts of financial frictions, pecuniary externalities arise and different distorsions appear, such as overborrowing, excessive risk-taking and excessive levels of short-term debt.[9] In these environments macroprudential intervention can improve social efficiency. An International Monetary Fund policy study argues that risk externalities between financial institutions and from them to the real economy are market failures that justify macroprudential regulation.[10]

In the mood swings paradigm, animal spirits (Keynes) critically influence the behavior of financial institutions' managers, causing excess of optimism in good times and sudden risk retrenchment on the way down. As a result, pricing signals in financial markets may be inefficient, increasing the likelihood of systemic trouble. A role for a forward-looking macroprudential supervisor, moderating uncertainty and alert to the risks of financial innovation, is therefore justified.

The cross-sectional dimension of risk can be monitored by tracking balance sheet information—total assets and their composition, liability (financial accounting) and capital structure—as well as the value of the institutions' trading securities and securities available for sale. Additionally, other sophisticated financial tools and models have been developed to assess the interconectedness across intermediaries (such as CoVaR[12]) and each institution's contribution to systemic risk (identified as "Marginal Expected Shortfall" in Acharya et al., 2011[13]).

To address the time dimension of risk, a wide set of variables are typically used, for instance: ratio of credit to GDP, real asset prices, ratio of non-core to core liabilities of the banking sector, and monetary aggregates. Some early warning indicators have been developed encompassing these and other pieces of financial data (see, e.g., Borio and Drehmann, 2009[14]). Furthermore, macro stress tests are employed to identify vulnerabilities in the wake of a simulated adverse outcome.

Most of these instruments are aimed to prevent the procyclicality of the financial system on the asset and liability sides, such as:

Using data from the UK, Aiyar et al. (2012)[18] find that unregulated banks in the UK have been able to partially offset changes in credit supply induced by time-varying minimum capital requirements over regulated banks. Hence, they infer a potentially substantial "leakage" of macroprudential regulation of bank capital.

In the sphere of emerging markets, several central banks have applied macroprudential policies (e.g., use of reserve requirements) at least since the aftermath of the 1997 Asian financial crisis and the 1998 Russian financial crisis. Most of these central banks' authorities consider that such tools effectively contributed to the resilience of their domestic financial systems in the wake of the late-2000s financial crisis.[19]

In analyzing the costs of higher capital requirements implied by a macroprudential approach, Hanson et al. (2011)[21] report that the long-run effects on loan rates for borrowers should be quantitatively small.[22]

Some theoretical studies indicate that macroprudential policies may have a positive contribution to long-run average growth. Jeanne and Korinek (2011),[23] for instance, show that in a model with externalities of crises that occur under financial liberalization, well-designed macroprudential regulation both reduces crisis risk and increases long-run growth as it mitigates the cycles of boom and bust.

Contents |

[edit] History

As documented by Clement (2010),[1] the term "macroprudential" was first used in the late 1970s in unpublished documents of the Cooke Committee (the precursor of the Basel Committee on Banking Supervision) and the Bank of England. But only in the early 2000s—after two decades of recurrent financial crises in industrial and, most often, emerging market countries[2]—did the macroprudential approach to the regulatory and supervisory framework become increasingly promoted, especially by authorities of the Bank for International Settlements. A wider agreement on its relevance has been reached as a result of the late-2000s financial crisis.[edit] Objectives and justification of macroprudential regulation

The main goal of macroprudential regulation is to reduce the risk and the macroeconomic costs of financial instability. It is recognized as a necessary ingredient to fill the gap between macroeconomic policy and the traditional microprudential regulation of financial institutions (Bank of England, 2009[3]).[edit] The macro and microprudential perspectives: understanding the difference

Following Borio (2003),[4] the macro- and microprudential perspectives differ in terms of their objectives and understanding on the nature of risk. Traditional microprudential regulation seeks to enhance the safety and soundness of individual financial institutions, as opposed to the macroprudential view which focuses on welfare of the financial system as a whole. Further, risk is taken as exogenous under the microprudential perspective, in the sense of assuming that any potential shock triggering a financial crisis has its origin beyond the behavior of the financial system. The macroprudential approach, on the other hand, recognizes that risk factors may configure endogenously, i.e. as a systemic phenomenon. In line with this reasoning, macroprudential policy addresses the interconnectedness of individual financial institutions and markets, as well as their common exposure to economic risk factors. It also focuses on the procyclical behavior of the financial system in the effort to foster its stability.

[edit] Theoretical rationale for macroprudential regulation

On theoretical grounds, it has been argued that a reform of prudential regulation should integrate three different paradigms:[5] the agency paradigm, the externalities paradigm, and the mood swings paradigm. The role of macroprudential regulation is particularly stressed by the last two of them.The agency paradigm highlights the importance of principal-agent problems. The main argument is that in its role of lender of last resort and provider of deposit insurance, the government alters the incentives of banks to undertake risks. This is a manifestation of the principal-agent problem known as moral hazard. More concretely, the coexistence of deposit insurances and insufficiently regulated bank portfolios induces financial institutions to take excessive risks.[6] This paradigm, however, assumes that risk arises from individual malfeasance, and hence it is at odds with the emphasis on the system as a whole which characterizes the macroprudential approach.

In the externalities paradigm, the key concept is called pecuniary externality. This is defined as an externality that arises when one economic agent's action affects the welfare of another agent through effects on prices. As argued by Greenwald and Stiglitz (1986),[7] when there are distorsions in the economy (such as incomplete markets or imperfect information[8]) policy intervention can make everyone better off in a Pareto efficiency sense. Indeed, a number of authors have shown that when agents face borrowing constraints or other sorts of financial frictions, pecuniary externalities arise and different distorsions appear, such as overborrowing, excessive risk-taking and excessive levels of short-term debt.[9] In these environments macroprudential intervention can improve social efficiency. An International Monetary Fund policy study argues that risk externalities between financial institutions and from them to the real economy are market failures that justify macroprudential regulation.[10]

In the mood swings paradigm, animal spirits (Keynes) critically influence the behavior of financial institutions' managers, causing excess of optimism in good times and sudden risk retrenchment on the way down. As a result, pricing signals in financial markets may be inefficient, increasing the likelihood of systemic trouble. A role for a forward-looking macroprudential supervisor, moderating uncertainty and alert to the risks of financial innovation, is therefore justified.

[edit] Indicators of systemic risk

In order to measure systemic risk, macroprudential regulation relies on several indicators. As mentioned in Borio (2003),[11] an important distinction is between measuring contributions to risk of individual institutions (the cross-sectional dimension) and measuring the evolution (i.e. procyclicality) of systemic risk through time (the time dimension).The cross-sectional dimension of risk can be monitored by tracking balance sheet information—total assets and their composition, liability (financial accounting) and capital structure—as well as the value of the institutions' trading securities and securities available for sale. Additionally, other sophisticated financial tools and models have been developed to assess the interconectedness across intermediaries (such as CoVaR[12]) and each institution's contribution to systemic risk (identified as "Marginal Expected Shortfall" in Acharya et al., 2011[13]).

To address the time dimension of risk, a wide set of variables are typically used, for instance: ratio of credit to GDP, real asset prices, ratio of non-core to core liabilities of the banking sector, and monetary aggregates. Some early warning indicators have been developed encompassing these and other pieces of financial data (see, e.g., Borio and Drehmann, 2009[14]). Furthermore, macro stress tests are employed to identify vulnerabilities in the wake of a simulated adverse outcome.

[edit] Macroprudential tools

A large number of instruments have been proposed;[15] however, there is no agreement about which one should play the primary role in the implementation of macroprudential policy.Most of these instruments are aimed to prevent the procyclicality of the financial system on the asset and liability sides, such as:

- Cap on loan-to-value ratio and loan loss provisions

- Cap on debt-to-income ratio

- Countercyclical capital requirement - to avoid excessive balance-sheet shrinkage from banks in trouble.

- Cap on leverage (finance) - to limit asset growth by tying banks' assets to their equity (finance).

- Levy on non-core liabilities - to mitigate pricing distorsions that cause excessive asset growth.

- Time-varying reserve requirement - as a means to control capital flows with prudential purposes, especially for emerging economies.

- Liquidity coverage ratio

- Liquidity risk charges that penalize short-term funding

- Capital requirement surcharges proportional to size of maturity mismatch

- Minimum haircut requirements on asset-backed securities

[edit] Implementation in Basel III

Several aspects of Basel III reflect a macroprudential approach to financial regulation.[16] Indeed, the Basel Committee on Banking Supervision acknowledges the systemic significance of financial institutions in the rules text. More concretely, under Basel III banks' capital requirements have been strengthened and new liquidity requirements, a leverage cap and a countercyclical capital buffer have been introduced. Also, the largest and most globally active banks are required to hold more and higher-quality capital, which is consistent with the cross-section approach to systemic risk.[edit] Effectiveness of macroprudential tools

For the case of Spain, Saurina (2009)[17] argues that dynamic loan loss provisions (introduced in July 2000) are helpful to deal with procyclicality in banking, as banks are able to build up buffers for bad times.Using data from the UK, Aiyar et al. (2012)[18] find that unregulated banks in the UK have been able to partially offset changes in credit supply induced by time-varying minimum capital requirements over regulated banks. Hence, they infer a potentially substantial "leakage" of macroprudential regulation of bank capital.

In the sphere of emerging markets, several central banks have applied macroprudential policies (e.g., use of reserve requirements) at least since the aftermath of the 1997 Asian financial crisis and the 1998 Russian financial crisis. Most of these central banks' authorities consider that such tools effectively contributed to the resilience of their domestic financial systems in the wake of the late-2000s financial crisis.[19]

[edit] Costs of macroprudential regulation

There is available theoretical and empirical evidence on the positive effect of finance on long-term economic growth. Accordingly, concerns have been raised about the impact of macroprudential policies on the dynamism of financial markets and, in turn, on investment and economic growth. Popov and Smets (2012)[20] thus recommend that macroprudential tools be employed more forcefully during costly booms driven by overborrowing, targeting the sources of externalities but preserving the positive contribution of financial markets to growth.In analyzing the costs of higher capital requirements implied by a macroprudential approach, Hanson et al. (2011)[21] report that the long-run effects on loan rates for borrowers should be quantitatively small.[22]

Some theoretical studies indicate that macroprudential policies may have a positive contribution to long-run average growth. Jeanne and Korinek (2011),[23] for instance, show that in a model with externalities of crises that occur under financial liberalization, well-designed macroprudential regulation both reduces crisis risk and increases long-run growth as it mitigates the cycles of boom and bust.

[edit] Institutional aspects

The macroprudential supervisory authority may be given to a single entity, existing (such as central banks) or new, or be a shared responsibility among different institutions (e.g., monetary and fiscal authorities). Illustratively, the management of systemic risk in the U.S. is centralized in the Financial Stability Oversight Council (FSOC), established in 2010. It is chaired by the United States Secretary of the Treasury and its members include the Chairman of the Federal Reserve System and all the principal U.S. regulatory bodies. In Europe, the task has also been assigned since 2010 to a new body, the European Systemic Risk Board (ESRB), whose secretariat is ensured by the European Central Bank. Differently from its U.S. counterpart, the ESRB lacks direct enforcement power.[edit] The role of central banks

In pursuing their goal of preserving price stability, central banks remain attentive to the evolution of real and financial markets. Thus, a complementary relationship between macroprudential and monetary policy has been advocated, even if the macroprudential supervisory authority is not given to the central bank itself. This is well reflected by the organizational structure of institutions such as the Financial Stability Oversight Council and European Systemic Risk Board, where central bankers have a decisive participation. The question of whether monetary policy should directly counter financial imbalances remains more controversial, although it has indeed been proposed as a tentative supplementary tool for addressing asset price bubbles.[24][edit] The international dimension of macroprudential regulation

On the international level, there are several potential sources of leakage and arbitrage from macroprudential regulation, such as banks' lending via foreign branches and direct cross-border lending.[25] Also, as emerging economies impose controls on capital flows with prudential purposes, other countries may suffer negative spillover effects.[26] Therefore, global coordination of macroprudential policies is considered as necessary to foster their effectiveness.[edit] See also

[edit] References

- ^ Clement, P. (2010). The term "macroprudential": origins and evolution. BIS Quarterly Review, March.

- ^ See Reinhart, C. and Rogoff, K. (2009). This time is different: Eight centuries of financial folly. Princeton University Press.

- ^ Bank of England (2009). The role of macroprudential policy. Bank of England Discussion Paper, November.

- ^ Borio, C. (2003). Towards a macro-prudential framework for financial supervision and regulation? BIS Working Papers No 128, February.

- ^ de la Torre, A. and Ize, A. (2009). Regulatory reform: Integrating paradigms. The World Bank. Policy Research Working Paper 4842.

- ^ See Kareken, J. and Wallace, N. (1978). Deposit insurance and bank regulation: A partial-equilibrium exposition, Journal of Business, 51: 413-438.

- ^ Greenwald, B. and Stiglitz, J. (1986). Externalities in economies with imperfect information and incomplete markets, Quarterly Journal of Economics, 101: 229-264.

- ^ http://www.econport.org/content/handbook/Imperfect-Information.html

- ^ For surveys in this literature, see e.g. Bianchi, J. (2010). Credit externalities: Macroeconomic effects and policy implications. American Economic Review: Papers & Proceedings, 100: 398-402; and Korinek, A. (2011). The new economics of prudential capital controls: A research agenda. University of Maryland. Mimeo.

- ^ De Nicolo, G., G. Favara and L. Ratnovski (2012). Externalities and macroprudential policy, IMF Staff Discussion Note 12/05.

- ^ Borio, C. (2003). Op.cit.

- ^ See Adrian, T. and Brunnermeier, M. (2011). CoVaR. NBER Working Papers 17454, National Bureau of Economic Research.

- ^ Acharya, V., Pederssen, L., Phillipon, T. and Richardson, M. (2010). Measuring Systemic Risk. New York University. Mimeo.

- ^ Borio, C. and Drehmann, M. (2009). Assessing the Risk of Banking Crises – Revisited. BIS Quarterly Review, March.

- ^ See, inter alia, Shin, H. (2011). Macroprudential policies beyond Basel III. In: BIS Papers No 60, December; Hanson, S., Kashyap, A. and Stein, J. (2011). A macroprudential approach to financial regulation. Journal of Economic Perspectives, 25: 3-28; Goodhart C. and Perotti, E. (2012). Preventive macroprudential policy. VoxEU.org, 29 February; and the references in Galati, G. and Moessner, R. (2011). Macroprudential policy -- a literature review. BIS Working Papers No 337, February.

- ^ See Borio, C. (2011). Rediscovering the macroeconomic roots of financial stability policy: journey, challenges and a way forward. BIS Working Papers No 354, September.

- ^ Saurina, J. (2009). Dynamic provisioning: The case of Spain. The World Bank. Note Number 7, July.

- ^ Aiyar, S., Calomiris, C. and Wieladek, T. (2011). Does Macro-Pru leak? Evidence from a UK policy experiment. NBER Working Papers 17822, National Bureau of Economic Research.

- ^ For the case of some Latin American countries, see e.g. Castillo, P., Contreras, A., Quispe, Z. and Rojas, Y. (2011). Política macroprudencial en los países de la región. In: Revista Moneda, Central Bank of Peru.

- ^ Popov, A. and Smets, F. (2012). On the tradeoff between growth and stability: The role of financial markets. VoxEU.org, 3 November.

- ^ Hanson, S., Kashyap, A. and Stein, J. (2011). A macroprudential approach to financial regulation. Journal of Economic Perspectives, 25: 3-28.

- ^ See also Schanz, J., Aikman, D., Collazos, P., Farag, M., Gregory, D. and Kapadia, S. (2011). The long-term economic impact of higher capital levels. In: BIS Papers No 60, December, as well as the references cited therein.

- ^ Jeanne, O. and Korinek, A. (2011). Booms, Bust and Growth. Johns Hopkins University and University of Maryland. Mimeo.

- ^ See Bernanke, B (2008). Monetary policy and the housing bubble. Speech at the Annual Meeting of the American Economic Association, Atlanta, Georgia. January 3, 2010.

- ^ Bank of England (2009), Op.cit.

- ^ Korinek, A. (2011), Op.cit.

[edit] Further reading and external links

- Conference Macroprudential regulation and policy (BIS - BoK, 2011), a collection of the articles presented during the conference "Macroprudential regulation and policy" jointly organised by the Bank for International Settlements and the Bank of Korea, on 16–18 January 2011.

- A literature review (Galati and Moessner, 2011)

- Report by the Working Group on Macroprudential Policy established by the Group of Thirty

- Financial Stability Oversight Council

- European Systemic Risk Board

No comments:

Post a Comment