Exploring mainly Heterodox type Economics, Monetary Reform, Environmental Sustainability, and Climate Change. It is a resource of Internet articles, and also promotes awareness of a futuristic modern universal Paradigm known as TFE, or Transfinancial Economics which is probably the most advanced, and most "scientific" form of Economics in the world .

As I mentioned yesterday, I spent six hours with Steve Keen yesterday. He cam down to see me in Ely, and we talked economics, MMT, annoying aspects of ageing and about his software programs, Minsky and Ravel.

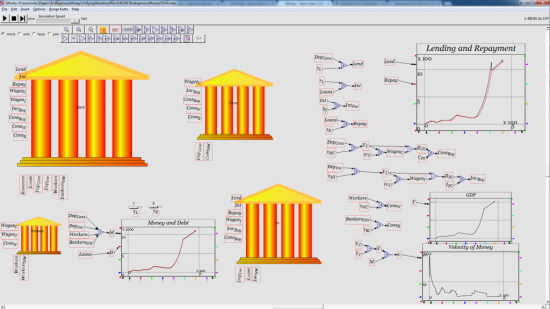

Minsky is an economic modelling tool built on the principles of double entry. It is open source and free. There is a manual of a couple of hundred pages. Anyone is free to have a go, but as we rapidly found, it's best not to try it on a Mac, where it only ‘sort of' works.

The process begins by defining the key players in the model that is being built. We looked at the function of central banks and so looked at the central bank, private banks, the Treasury and the private sector economy (which was a bit of a catch all that could clearly be expanded).

Then you define the flows each might make e.g. government spending, taxes, bond issues, bond redemptions and repurchases, interest paid and so on, plus similar flows in the private sector e.g. loans and interest, etc.

The model has to balance: critically, you are not allowed to make single entries (or rather, you are, but the model will make clear that it does not work, so you have to put them right). Given that most government accounting is single entry and most macro does not really recognise the role of money in the economy, this is in itself quite revolutionary stuff.

Then Steve worked forward, explaining how relationships between variables can be defined within parameters so that behaviour can be predicted. You begin to end up with screens looking like this:

Charting results is one of the easier things to do.

I make no pretence that I have learned the programme as yet. There is syntax that I have been introduced to, but I suspect have not mastered as yet. And there were methods used that I am bound to forget until I try it for myself and have to rediscover them - although at least I know they are there, somewhere, now. That seems a little daunting, but so too did computer aided design (CAD) when I first tried to use it, and now I am pretty good with it and have little difficulty thinking of ways to sort out issues. I suspect Minsky will be like that.

I actually think the comparison between CAD and Minsky might be quite appropriate. Both provide toolboxes and a workspace. What you do thereafter is up to you. If you have nothing you want to design using CAD there is no point learning it. If you have nothing in the economy that you want to model the effort spent learning Minsky would also be a waste of time.

What might I model? I was sufficiently excited by this model to lose sleep over it last night, something I am not inclined to do very often. Thoughts on what to model included:

The problem of accounting for government interest costs in a period of inflation - which involves no known double entry in the way that the ONS does it.

Accounting for government debt itself, which again is based on rather dubious single entry accounting in the way that the ONS do it.

Modelling tax revenues and multiplier effects within them. Linking this to GDP would also be good. Linking it to wheat makes up GDP might be even better.

Modelling central bank digitise currencies and what that would demand that the government get its head around.

I am certain there is a great deal more.

Ravel is a digital data display program that lays over Minsky. It is not open source or free. It looks to be very powerful. For those familiar with it, Tableu looks to be what it approximates to. For me I can see massive uses for it. Steve is giving me a copy.

However, all this requires an investment in a decent PC, because this requires i7 processing power and decent graphic cards I think, plus good storage to read and write what look like they could become pretty big files. That's my question for the day. Do I fork out now and break more than 12 years working solely on the Mac?

I will let you know. But the temptation is very a strong. These programs will let me look at issues in new ways. And that is always exciting. And it is for precisely this type of investment that I accept donations on the blog.

( Blogger comment Though interesting to some degree it is no match to the kind of understanding of the economy as understood in Transfinancial Economics).

Last week I made my first overseas trip on which I ticked the box 'Australian resident departing permanently'. It’s given me cause to reflect on my career as an academic economist (and part-time journalist) in Australia.

Today I commence a new role as Head of the School of Economics, History and Politics atKingston University, London, 41 years after my life as an economist began in 1973. That’s not when my PhD was approved, nor when I got my first academic job, but the date on which I participated in the student revolt over the teaching of economics in a dispute that led to the formation of the Department of Political Economy at Sydney University in 1975.

This dispute has always been tagged with a left-wing brush. Australia’s current Prime Minister Tony Abbott, when he was President of the Students Representative Council at Sydney University in 1979, supported cutbacks to University funding on the grounds that they would force Universities to stop running courses like political economy:

Abbott: “Quite frankly I think that these courses are not only trivial, but they are attempts by unscrupulous academics to impose simplistic ideological solutions upon students, as it were to make students the cannon fodder for their own private versions of the revolution. And I think that if there were further cuts to the education budget well then we would certainly see the Universities cracking down on that sort of course. The fact that they can offer that sort of course is to me proof that there is room for further cuts.”

Interviewer: “You also suggest cutting out political economy?”

There’s no doubt that the vast majority of the activists in Political Economy Movement were left-wing. But my core motivation for taking part in that dispute was that mainstream economic theory was simply wrong.

The next 40 years of reading economic literature confirmed that gut feeling. Mainstream ‘neoclassical’ economics had a multitude of flaws, all of which had been documented in the academic literature, yet almost none of them were discussed in economics textbooks.

Instead, textbook authors either ignored the problems, or did the mother of all Photoshop jobs on the frankly ludicrous assumptions that were made to paper over problems in the theory, so that the flawed models could sound halfway reasonable to someone who only read the textbooks.

I decided that the best way to reform economics was to explain the technical problems in economic theory in a way that a non-mathematical audience could understand, and to “read aloud the dirty bits” as well: to publish the unsanitised assumptions as they were made in the journals themselves. Statements like the following, for example:

The necessary and sufficient condition quoted above is intuitively reasonable. It says, in effect, that an extra unit of purchasing power should be spent in the same way no matter to whom it is given. (Gorman 1953 , p. 64)

“Intuitively reasonable”? Delusional is closer to it.

But explaining that the theory was unsound wasn't enough. There had to be an alternative way of thinking about the economy too that actually made sense, and there also had to be a reason for the public to actually worry about the state of economic theory in the first place.

I found the explanation that in Hyman Minsky’s John Maynard Keynes, which is not a biography. Most non-orthodox economics portrayed capitalism as having a tendency towards stagnation. In contrast, Minsky saw the fundamental instability in a capitalist system as upwards: “The tendency to transform doing well into a speculative investment boom is the basic instability in a capitalist economy.”

Banks, private debt, asset markets and money played essential roles in Minsky’s vision of capitalism, but they were completely ignored in mainstream economic models before the crisis. This is where Abbott was and is wrong: just because left-wing economists are ideological, it doesn’t follow that mainstream economics was logical. Crucially, its illogical decision to model capitalism as if banks, private debt and money didn’t exist led it massively astray when it came to perceive grave risks to the real economy.

Minsky’s realistic vision of capitalism instead indicated that a pure free market economy --one with no government sector at all -- could collapse into a terminal debt-deflation after a series of debt-driven booms and subsequent slumps. On the other hand, a mixed economy in which government was a substantial economic force whose net spending rose when the economy went into a slump would avoid a debt-deflation, but it would necessarily be cyclical, though with milder booms and slumps.

In 1992, I modelled Minsky by adding two elements of realism to Richard Goodwin’s highly stylised model of a cyclical economy. In Goodwin’s model, capitalists invested all their profits, while workers made wage demands depending on the level of employment. I added the reality that capitalists invest less than profits during a slump, but more than profits than a boom, with the extra finance being created by bank lending.

Figure 1: The "black hole of debt" in my 1992 model

My mixed economy model included a government sector that defended a target level of employment spent more than taxes during slumps and less than taxes during booms, and financed this by its own money-creation capability.

The two models generated the outcomes Minsky anticipated, but the real world fitted neither of these models precisely. So I expected the real world to display a mixture of the results of the two models. As I put it in my 1995 paper: "Increased government spending during slumps would enable recovery in the aftermath to lesser booms; larger booms, however, could result in the rate of growth of accumulated private debt exceeding net profits for some time, thus leading to a prolonged slump."

Figure 2: The cyclically stable mixed economy 1992 model

So I had an alternative way of thinking about the economy, which cautioned against the many radical ‘reforms’ of capitalism that the neoclassical school was gung-ho about: deregulating finance, reducing the size of the government sector, eliminating trade unions, driving inflation towards zero. From my “Minskian” perspective, what they were doing was making the real world less like the cyclical but stable system shown in Figure 2and more like the superficially stable but ultimately catastrophic system shown in Figure 1. I therefore felt that the economy could quite possibly fall into a serious economic crisis which would take the mainstream utterly by surprise. One look at the private debt data for Australia and the USA in 1995 (see Figure 3) convinced me that a crisis was certain in the near future -- and too soon to tolerate the lengthy publication delays that occur in the academic press. So I turned to the media and to the blogosphere.

Figure 3: Australian & US private debt ratios when I started to warn of an impending crisis

That crisis duly occurred about two years later, and took mainstream economics completely by surprise, because neoclassical economic models then completely ignored the role of banks, private debt, and money. They instead focused on the levels of employment and inflation, and saw the apparent stability of the ‘Great Moderation’ as indicators that they have finally tamed the business cycle:

"There is evidence for the view that improved control of inflation has contributed in important measure to this welcome change in the economy." (Bernanke 2004, “What Have We Learned Since October 1979?”)

Figure 4: The crisis began when the rate of growth of private debt slowed down

The crisis shook mainstream policy economists to the core, and led to the biggest government economic rescue operation since the Great Depression. It was a scale of engagement that took me by surprise, until I realised that the rescue policies were driven not by economic theory but by sheer, blind panic:

“We need to buy hundreds of billions of assets”, I said. I knew better than to utter the word trillion. That would have caused cardiac arrest. “We need an announcement tonight to calm the market, and legislation next week,” I said.

What would happen if we didn’t get the authorities we sought, I was asked.

As it turned out, sheer blind panic was a better guide to what to do in a crisis than was economic theory. The immense injection of government money stopped the downward plunge into Depression—as Minsky had argued that it would.

But then the human psyche came into play. Mainstream academic economists excused themselves from their failure to anticipate the crisis with the mantra that “no-one could have seen this coming”, politicians and policy economists went back to obsessing about the level of government debt, and ignoring the dynamics of private debt, and another private-debt-driven boom began in the Anglo countries (see Figure 5).

Figure 5: Today's recovery is driven by rising private debt from an unprecedented level after a slump

So business-as-usual has returned. But it won’t be business-as-usual at Kingston. I’ve been hired with the express mandate to take a University that is open to non-orthodox thought in economics and make it even stronger. We will teach neoclassical economics as well, warts and all. And we will teach the many non-orthodox streams of thought (post Keynesian, evolutionary economics, econophysics) too.

In doing so, we’ll be responding to the successors of those students who, 41 years ago, fought for a different approach to economics at Sydney University. There are now at least 65 student organizations around the world calling for a new approach to economics in what they have titled ISIPE: the "International Student Initiative for Pluralism in Economics”.

Today’s mainstream economists will surely regard them as hopelessly ill-informed about economic theory. They are not. They simply want a realistic approach to economics, as I did when I was in their shoes 41 years ago.

Steve Keenis author of Debunking Economics and the blog Debtwatch and developer of the Minsky software program. A longer version of this article will be published on Debtwatchlater this week.

The following intro is a short account of Hyman Minksy from Radio 4 (BBC). A link is also included at the end of it which should lead to a radio programme of his life, and work. The Blogger who is the originator of Transfinancial Economics wishes to make the point that TFE ofcourse recognizes Minky's basic claim that the stability in the economy can be distabilising, and uncertain. It's super flexible electronic controls over the economy could be programmed in such a way as to deal with such uncertainty in Real-Time. To understand this more clearly it would be advisable to go to the following link http://www.p2pfoundation.net/Transfinancial_Economics

American economist Hyman Minsky died in 1996, but his theories offer one of

the most compelling explanations of the 2008 financial crisis. His key idea is

simple enough to be a t-shirt slogan: "Stability is destabilising". But TUC

senior economist Duncan Weldon argues it's a radical challenge to mainstream

economic theory. While the mainstream view has been that markets tend towards

equilibrium and the role of banks and finance can largely be ignored, Minsky

argued that in the good times the seeds of the next crisis are sown as the

financial sector engages in riskier and riskier lending in pursuit of profit. In

the aftermath of the financial crisis, this might seem obvious - so why did

Minsky die an outsider? What do his ideas say about the response to the 2008

crisis and current policies like Help to Buy? And has mainstream economics done

enough to respond to its own failure to predict the crisis and the challenge

posed by Minsky's ideas?

Hyman Philip Minsky (September 23, 1919 – October 24, 1996) was an Americaneconomist, a professor of economics at Washington University in St. Louis, and a distinguished scholar at the Levy Economics Institute of Bard College. His research attempted to provide an understanding and explanation of the characteristics of financial crises, which he attributed to swings in a potentially fragile financial system. Minsky is sometimes described as a post-Keynesian economist because, in the Keynesian tradition, he supported some government intervention in financial markets, opposed some of the financial deregulation policies popular in the 1980s, stressed the importance of the Federal Reserve as a lender of last resort and argued against the over-accumulation of private debt in the financial markets.[1]

Minsky was a consultant to the Commission on Money and Credit while he was an Associate Professor of Economics at the University of California, Berkeley.

Minsky proposed theories linking financial market fragility, in the normal life cycle of an economy, with speculativeinvestment bubblesendogenous to financial markets. Minsky claimed that in prosperous times, when corporate cash flow rises beyond what is needed to pay off debt, a speculative euphoria develops, and soon thereafter debts exceed what borrowers can pay off from their incoming revenues, which in turn produces a financial crisis. As a result of such speculative borrowing bubbles, banks and lenders tighten credit availability, even to companies that can afford loans, and the economy subsequently contracts.

This slow movement of the financial system from stability to fragility, followed by crisis, is something for which Minsky is best known, and the phrase "Minsky moment" refers to this aspect of Minsky's academic work.

"He offered very good insights in the '60s and '70s when linkages between the financial markets and the economy were not as well understood as they are now," said Henry Kaufman, a Wall Street money manager and economist. "He showed us that financial markets could move frequently to excess. And he underscored the importance of the Federal Reserve as a lender of last resort."[4]

Minsky's model of the credit system, which he dubbed the "financial instability hypothesis" (FIH),[5] incorporated many ideas already circulated by John Stuart Mill, Alfred Marshall, Knut Wicksell and Irving Fisher.[6] "A fundamental characteristic of our economy," Minsky wrote in 1974, "is that the financial system swings between robustness and fragility and these swings are an integral part of the process that generates business cycles."[7]

Disagreeing with many mainstream economists of the day, he argued that these swings, and the booms and busts that can accompany them, are inevitable in a so-called free market economy – unless government steps in to control them, through regulation, central bank action and other tools. Such mechanisms did in fact come into existence in response to crises such as the Panic of 1907 and the Great Depression. Minsky opposed the deregulation that characterized the 1980s.

It was at the University of California, Berkeley that seminars attended by Bank of America executives helped him to develop his theories about lending and economic activity, views he laid out in two books, John Maynard Keynes (1975), a classic study of the economist and his contributions, and Stabilizing an Unstable Economy (1986), and more than a hundred professional articles.

Minsky's theories have enjoyed some popularity, but have had little influence in mainstream economics or in central bank policy.

Minsky stated his theories verbally, and did not build mathematical models based on them. Consequently, his theories have not been incorporated into mainstream economic models, which do not include private debt as a factor. The post-Keynesian economist Steve Keen has recently developed models of endogenous economic crises based on Minsky's theories, but they are currently at the research stage and do not enjoy widespread use.[8]

Minsky's theories, which emphasize the macroeconomic dangers of speculative bubbles in asset prices, have also not been incorporated into central bank policy. However, in the wake of the financial crisis of 2007–2010 there has been increased interest in policy implications of his theories, with some central bankers advocating that central bank policy include a Minsky factor.[9]

Minsky's theories and the subprime mortgage crisis[edit]

Hyman Minsky's theories about debt accumulation received revived attention in the media during the subprime mortgage crisis of the late 2000s.[10]

Minsky argued that a key mechanism that pushes an economy towards a crisis is the accumulation of debt by the non-government sector. He identified three types of borrowers that contribute to the accumulation of insolvent debt: hedge borrowers, speculative borrowers, and Ponzi borrowers.

The "hedge borrower" can make debt payments (covering interest and principal) from current cash flows from investments. For the "speculative borrower", the cash flow from investments can service the debt, i.e., cover the interest due, but the borrower must regularly roll over, or re-borrow, the principal. The "Ponzi borrower" (named for Charles Ponzi, see also Ponzi scheme) borrows based on the belief that the appreciation of the value of the asset will be sufficient to refinance the debt but could not make sufficient payments on interest or principal with the cash flow from investments; only the appreciating asset value can keep the Ponzi borrower afloat.

If the use of Ponzi finance is general enough in the financial system, then the inevitable disillusionment of the Ponzi borrower can cause the system to seize up: when the bubble pops, i.e., when the asset prices stop increasing, the speculative borrower can no longer refinance (roll over) the principal even if able to cover interest payments. As with a line of dominoes, collapse of the speculative borrowers can then bring down even hedge borrowers, who are unable to find loans despite the apparent soundness of the underlying investments.[5]

Applying the hypothesis to the subprime mortgage crisis[edit]

Economist Paul McCulley described how Minsky's hypothesis translates to the subprime mortgage crisis.[11] McCulley illustrated the three types of borrowing categories using an analogy from the mortgage market: a hedge borrower would have a traditional mortgage loan and is paying back both the principal and interest; the speculative borrower would have an interest-only loan, meaning they are paying back only the interest and must refinance later to pay back the principal; and the ponzi borrower would have a negative amortization loan, meaning the payments do not cover the interest amount and the principal is actually increasing. Lenders only provided funds to ponzi borrowers due to a belief that housing values would continue to increase.

McCulley writes that the progression through Minsky's three borrowing stages was evident as the credit and housing bubbles built through approximately August 2007. Demand for housing was both a cause and effect of the rapidly-expanding shadow banking system, which helped fund the shift to more lending of the speculative and ponzi types, through ever-riskier mortgage loans at higher levels of leverage. This helped drive the housing bubble, as the availability of credit encouraged higher home prices. Since the bubble burst, we are seeing the progression in reverse, as businesses de-leverage, lending standards are raised and the share of borrowers in the three stages shifts back towards the hedge borrower.

McCulley also points out that human nature is inherently pro-cyclical, meaning, in Minsky's words, that "from time to time, capitalist economies exhibit inflations and debt deflations which seem to have the potential to spin out of control. In such processes, the economic system's reactions to a movement of the economy amplify the movement – inflation feeds upon inflation and debt-deflation feeds upon debt deflation." In other words, people are momentuminvestors by nature, not value investors. People naturally take actions that expand the high and low points of cycles. One implication for policymakers and regulators is the implementation of counter-cyclical policies, such as contingent capital requirements for banks that increase during boom periods and are reduced during busts.

Jump up ^pg. 14, Manias, Panics, and Crashes, 4th Ed. by Charles P. Kindleberger

Jump up ^Minsky, Hyman P. (1974). "The Modeling of Financial Instability: An introduction". Modeling and Simulation. Proceedings of the Fifth Annual Pittsburgh Conference 5.

Jump up ^Are we "It" yet?, by Steve Keen, Associate Professor in economics and finance at the University of Western Sydney, July 3rd, 2010